Browse categories

Explore

Fiverr Pro

English

$

USD

Automating trading strategies with Python, MQL5, and Pine Script

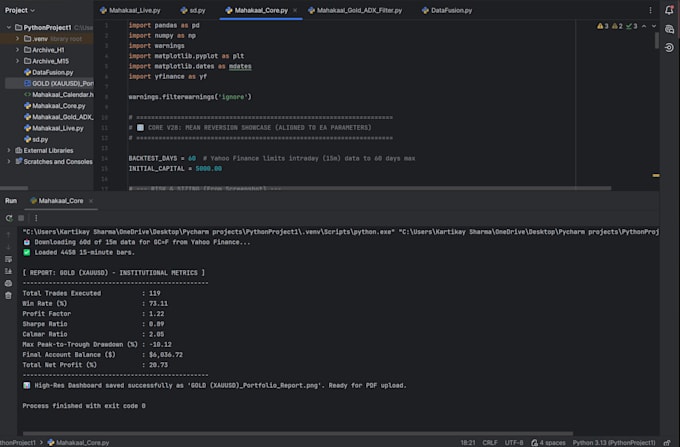

Before you risk real capital on a manual strategy or an automated bot, you must prove that your logic has a mathematical edge.

I will build a custom Python engine to rigorously analyze your trading strategy against historical market data. I specialize in quantitative analysis strictly for the Forex, Cryptocurrency, and Commodities markets (such as XAUUSD).

What I will do for you:

Depending on your chosen package, your quantitative report will include:

Stop guessing and start trading with statistical proof. Send me a message with your strategy rules, and let's validate your edge!

Platform:

TradingView

•

MT5

•

Binance

Development technology:

Python

•

PineScript

•

MQL5

Do I need to share my exact strategy rules with you? Is it safe?

Yes, I need your precise entry, exit, risk management, and indicator rules to code the simulation model. Your intellectual property is 100% safe, secure, and kept strictly confidential. I am more than happy to sign a Non-Disclosure Agreement (NDA) before we begin.

What asset classes do you specialize in for this service?

I specialize strictly in global Forex currency pairs, Cryptocurrencies (like BTC and ETH), and Commodities (such as Gold/XAUUSD). I focus heavily on these markets to ensure the highest quality historical data modeling.

If the data shows my strategy is profitable, can you turn it into a bot?

Absolutely. If the performance report reveals a strong mathematical edge and you want to fully automate it, we can easily transition into building a custom automated trading bot or Expert Advisor (EA) via my dedicated development gig.

How do you ensure the historical data analysis is accurate?

I use high-quality, institutional-grade historical data and clean it using Python. My testing architecture is designed to completely avoid common simulation traps like look-ahead bias or indicator "repainting," giving you realistic metrics you can actually trust.